Monthly Market Commentary - August 2023

Monthly Market Commentary - August 2023

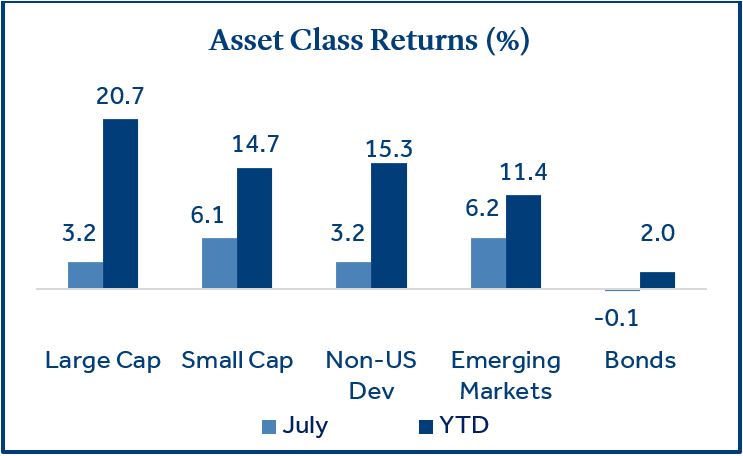

Market Update

Equities add to year-to-date gains while bonds regress.

Equity returns were positive across the spectrum in July as investors raised expectations for a soft-landing for the U.S. economy. During July, inflation continued its downward trajectory, job growth remained strong, and early indications were that corporate earnings would remain resilient. Against this backdrop, small-cap stocks (Russell 2000 Index) outperformed large-cap stocks (S&P 500 Index) for the 2nd month in a row as lower inflation and widening market strength served as a tailwind for smaller stocks. Bonds declined modestly as yields were slightly higher for the month. Lastly, emerging markets stocks (MSCI EM Index) outperformed U.S. and non-U.S. developed market stocks (MSCI EAFE Index) amid a declining U.S. dollar and optimism the Fed is nearing the end of the current rate hike cycle.

Federal Reserve

The Fed resumed interest rate increases following a brief pause.

After the brief pause in June, the Federal Reserve (the Fed) increased short-term lending rates by 0.25% in late-July. The committee believed that waiting longer to raise rates again would have increased the risk of reheating inflation. Although the Consumer Price Index (CPI) continues to trend lower, it still sits above the Fed’s desired target of 2%. Headline CPI for June registered 3.0% year-over-year, well below the prior month (4.0%), and less than half (6.5%) of where it ended 2022. Used cars, airfares, and household furnishings all declined while food prices remained stable.

Following the announcement, Fed Chair Jerome Powell commented that recent economic activity had expanded at a moderate pace, the labor market remained strong, while inflation remained elevated. He expressed the Fed will be highly attentive to inflation risks and any future rate hikes will be data dependent. The market reaction was muted as the increase was well telegraphed and in-line with market expectations. Although the Fed left the door open for additional rate hikes, the futures market currently forecasts the Fed funds rate will remain at current levels through the end of 20231.

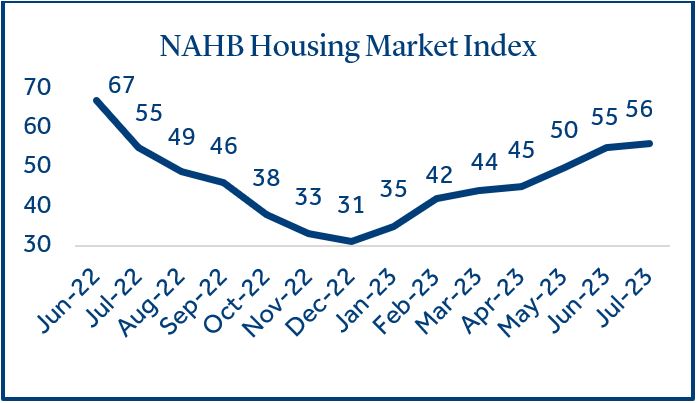

Real Estate

The housing market is showing signs of a steady recovery.

The U.S. housing market has been an area of strength this year even as the overall economic landscape has been jumbled. This could be good news for investors as the U.S. housing market represents 15-18% of domestic GDP2. Housing contributes to growth in multiple ways such as residential investment (new construction), housing services (rents and utilities), and home furnishings. Following a challenging environment in 2022, there has been a steady recovery in homebuilder expectations in 2023. Homebuilder sentiment is a leading economic indicator and may suggest additional strength in housing over the course of the year.

Commercial Real Estate has received attention as an area of potential risk to economic growth, as urban office buildings have struggled to maintain capacity in the post-Covid work environment. In fact, Office Real Estate Investment Trusts (REITs) have been a laggard in the real estate sector, returning -6% year-to-date. However, office space only represents 15%3 of the commercial real estate market and other sectors have performed more favorably this year with REITs overall returning +5%.

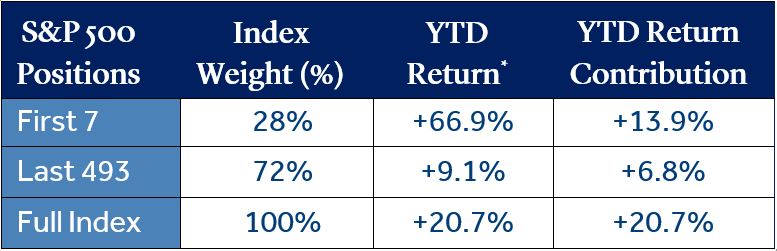

Equity Market Breadth

Narrow leadership has driven gains in the S&P 500 year-to-date.

Dubbed the “magnificent seven”, the stocks of tech companies Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla are currently the largest positions in the S&P 500 Index and comprise approximately 28% of the large-cap benchmark. More importantly to investors, these seven stocks had an index-weighted average return of 67% year-to-date through July 31 and account for two-thirds of the gains in the index this year.

Despite weaker breadth in returns to start 2023, there are signs that smaller, cyclical-oriented stocks are beginning to gain momentum. In June and July, mid- and small-cap stocks out-gained large-cap stocks over two consecutive months. In addition, more economically sensitive and value-oriented sectors such as Energy, Industrials, and Materials outperformed in July and could be signaling a rotation and the potential for new market leadership.

* Weighted average return calculated in FactSet.

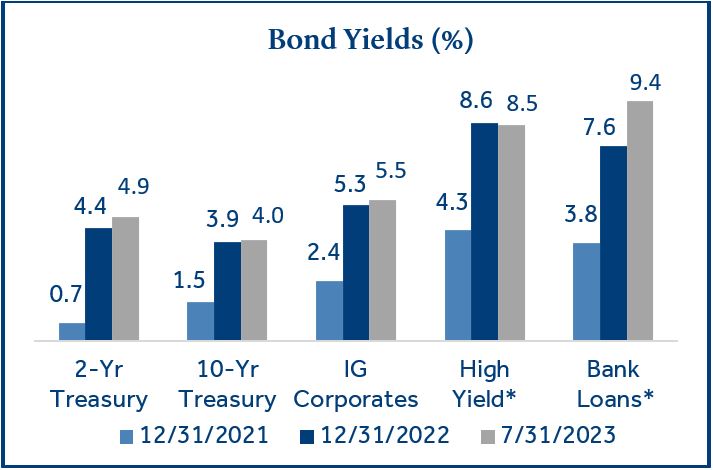

Fixed Income

Bond yields are at their highest level in years.

While equities have garnered most of the attention for their strong returns in 2023, it’s hard to ignore the rise in bond yields that coincided with the Fed’s interest rate hiking cycle. Although bonds haven’t generated the same level of returns as stocks year-to-date, they have rebounded, and yields are as attractive as they’ve been in some time.

For many years following the "Great Financial Crisis" in 2008, the Fed's monetary (interest rate) policy was the key tool used to repair the economy. The Fed used its authority to hold short-term rates near 0% for more than a decade in an attempt to spur economic growth after the U.S. housing collapse. During the period since the crisis, investors became accustomed to low interest rates and low bond yields. A new dynamic has unfolded in 2023 as bonds are once again an attractive source of portfolio return. Current yields for certain sectors are at decade-high levels. Higher bond yields haven't been widely available in recent years and therefore bonds could be particularly enticing to income-oriented investors or those looking to add diversification to equity heavy portfolios.

* Non investment grade (BB rating or below)

Economic Calendar

Payroll data could drive the market narrative in August.

Nonfarm payrolls and unemployment will be highly anticipated by investors early in the month. The job market remains resilient, and payrolls were steady in June, but growth was below expectations. It could be a situation where investors are looking for a “goldilocks” type number (not too hot and not too cold), enough job growth to avoid a recession but not strong enough to reignite inflation. A moderate labor report would likely support the case for a soft landing for the U.S. economy.

Things will get busier mid-month as we get the release of the Consumer Price Index (CPI), retail sales, and the latest from the Fed.

Data and rates used were indicative of market conditions as of the date shown. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions and are subject to change without notice. This material is intended for general public use and is for educational purposes only. By providing this content, Park Avenue Securities LLC is not undertaking to provide any recommendations or investment advice regarding any specific account type, service, investment strategy or product to any specific individual or situation, or to otherwise act in any fiduciary or other capacity. Please contact a financial professional for guidance and information that is specific to your individual situation. Indices are unmanaged and one cannot invest directly in an index. Links to external sites are provided for your convenience in locating related information and services. Guardian, its subsidiaries, agents, and employees expressly disclaim any responsibility for and do not maintain, control, recommend, or endorse third-party sites, organizations, products, or services and make no representation as to the completeness, suitability, or quality thereof. Past performance is not a guarantee of future results.

Capital Market Return sourced from Morningstar Direct. Asset categories listed correspond to the following underlying indices: Large-cap (S&P 500), Small-cap (Russell 2000), Non-US Dev (MSCI EAFE), Emerging Markets (MSCI EM), Bonds (Bloomberg US Aggregate Bond).

Treasury Yields sourced from the U.S. Department of the Treasury. IG (Investment Grade) Corporates, High Yield and Bank Loan yields sourced from Morningstar Direct.

1 Source: CME FedWatch Tool

2 Source: National Association of Home Builders

3 Source: Morningstar

NAHB Housing Market Index is based on a monthly survey to NAHM (National Association of Home Builders) members designed to take the pulse of the single-family housing market. Respondents rate conditions for the sale of new homes as well as traffic of prospective buyers.

Durable Goods, Retail Sales, Nonfarm Payrolls, and unemployment rate data sourced from Trading Economics.

Durable Goods measure the cost of orders received by U.S. manufacturers of goods meant to last at least three years.

Retail Sales represents the level of retail sales directly to U.S. consumers.

The Consumer Price Index (CPI) examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care and is a commonly used measure of the rate of inflation.

Fund Funds Rate: Short-term target interest rate set by the Federal Open Market Committee (FOMC); the policy making committee of the Federal Reserve. It’s the interest that banks and other depository institutions lend money on an overnight basis.

S&P 500 Index: Index is generally considered representative of the stock market as a whole. The index focuses on the large-cap segment of the U.S. equities market.

Russell 2000 Index: Index measures performance of the small-cap segment of the U.S. equity universe.

MSCI EAFE Index: Index measures the performance of the large and mid-cap segments of developed markets, excluding the U.S. & Canada.

MSCI EM Index: Index Measures the performance of the large and mid-cap segments of emerging market equities.

Bloomberg U.S. Aggregate Bond Index: Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS, ABS, and CMBS.

Park Avenue Securities LLC (PAS) is a wholly owned subsidiary of The Guardian Life Insurance Company of America

(Guardian). PAS is a registered broker-dealer offering competitive investment products, as well as a registered investment advisor offering financial planning and investment advisory services. PAS is a member of FINRA and SIPC.

2023-159169 (Exp. 7/25)