Monthly Market Commentary - August 2024

Monthly Market Commentary - August 2024

Market Update

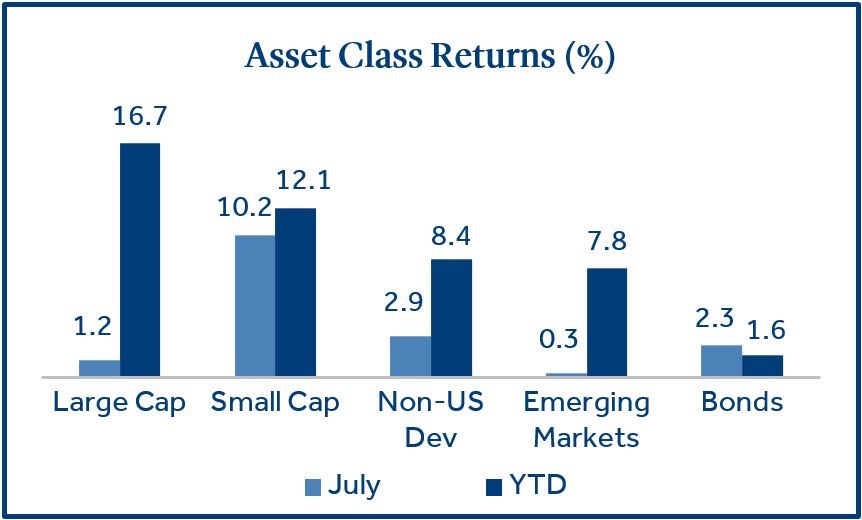

U.S. small cap stocks gained momentum in July on constructive economic data.

Small caps posted strong returns in July while most other stock indices increased modestly. Better than expected Q2 gross domestic product (+2.8%) and cooler than expected inflation (+3.0%) paved the way for improving sentiment for small caps. Against this backdrop:

- Small cap stocks posted their strongest monthly return of 2024: Small caps (Russell 2000 Index) gained +10.2% and outperformed large caps (S&P 500 Index) which returned +1.2%. The positive return difference between small caps and large caps of +9.0% in July was the widest in over ten years1.

- Bonds have made gains in three straight months: Bonds (Bloomberg US Aggregate Bond Index) returned +2.3% as interest rates moved lower. The 10-year U.S. Treasury yield declined from 4.36% to 4.09% (-0.27%) during the month.

- Non-U.S. developed markets outpaced EM stocks: Non-U.S. developed market stocks (MSCI EAFE Index) gained +2.9% and outperformed EM stocks (MSCI EAFE Index) which returned +0.3%. UK stocks helped boost developed market returns due to hopes that lower interest rates and political stability could provide a positive set up for UK equities.

U.S. Equities

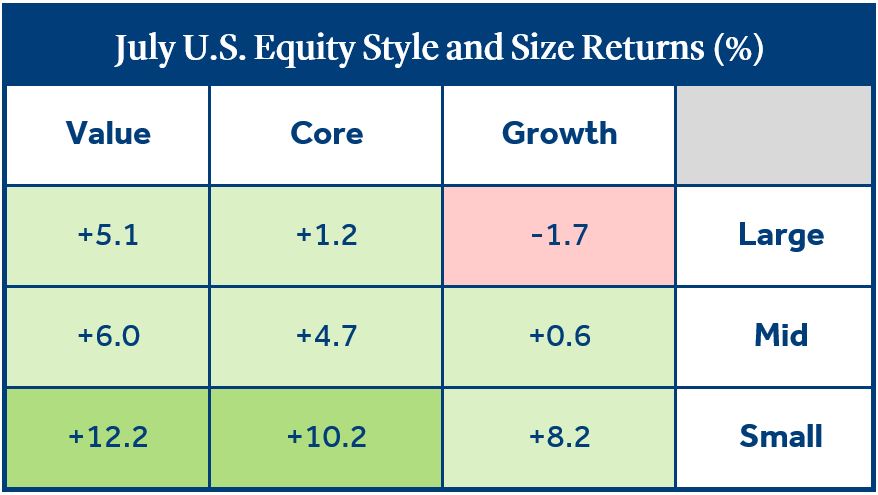

Investors rotated from large caps into small caps as expectations for interest rate cuts increased.

Investor sentiment shifted significantly during July as several underperforming areas from the first half of the year demonstrated improvement. Small caps, value-oriented stocks, and dividend paying stocks all posted strong returns while mega cap technology stocks, which have led markets higher over the last 18 months, lost momentum.

- Small cap stocks led U.S. equity returns in July: The shift in sentiment from large cap growth stocks into small cap stocks in July was dubbed the “great rotation”. Inflation declined from 3.5% in March to 3.0% in June and is expected to provide the Federal Reserve (Fed) with the evidence necessary to lower interest rates later this year. Small cap stocks frequently outperform large cap stocks in periods following the Fed’s initial rate cut2.

- Value stocks gain ground on growth stocks: Value stocks across market capitalizations (size) benefited from the rotation out of growth stocks. Higher yielding dividend paying value stocks are likely more attractive to investors with the potential for interest rates to move lower. In addition, political rhetoric around tougher export restrictions on U.S. technology companies to China and uncertainty around U.S.-Taiwan relations dampened enthusiasm for mega-cap technology stocks.

Fixed Income

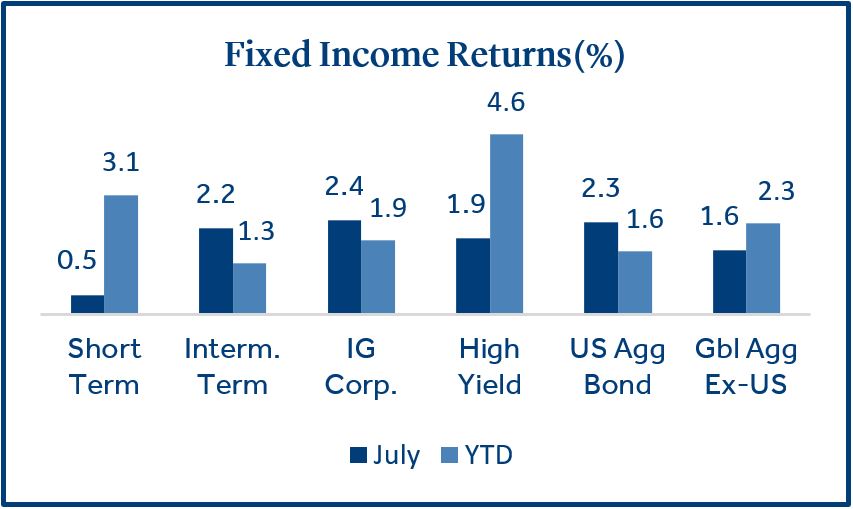

Fixed income sectors continued to benefit from lower Treasury yields.

Positive economic growth, cooling inflation, and expectations for interest rate cuts in 2024 have guided bonds to a three-month win streak for the first time since 2021. During this time, the 10-year U.S. Treasury yield has declined meaningfully from 4.70% to 4.09%.

- Long duration bonds outperformed short duration bonds: Longer-term bonds have benefitted from falling Treasury yields over the past three months and have been closing the gap year-to-date versus shorter-term bonds. When the Fed eventually lowers short-term rates, money market yields will likely adjust lower rapidly as they have historically been highly correlated with the Fed Funds rate.

- Investment grade (IG) corporate bonds led fixed income returns in July: IG corporate bonds (rated BBB and above) have benefited from higher yields (+5.3)% compared to like Treasury bonds (+4.01%) and longer duration (7 years) versus high yield bonds (3 years).

- Fidelity and MFS maintained their positive outlook for bonds: Fidelity stated in their mid-year outlook that “it has been almost 20 years since bonds presented as attractive an opportunity as they are likely to in the second half of 2024” and MFS recently reiterated their overweight to bonds (versus equities), due to their attractive risk-adjusted return potential.

U.S. Presidential Election

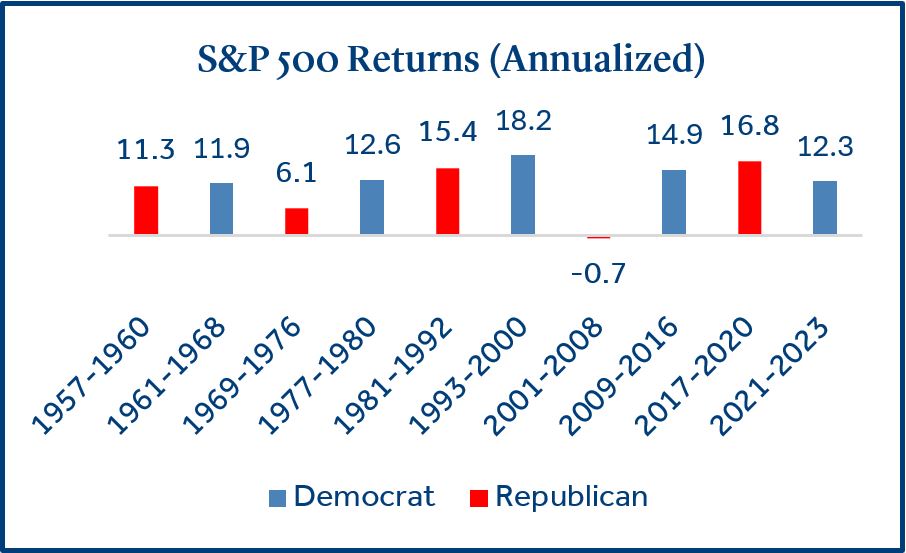

Political volatility in the U.S. reached extreme levels in July.

July represented a highly tumultuous month for the U.S. presidential race. On July 13, former President Donald Trump survived an assassination attempt at a campaign rally in Pennsylvania. Just eight days later, standing President Joe Biden ended his 2024 candidacy with only four months until the election.

- Recent polls suggest the election may come down to the wire: With less than 100 days until the election, recent data has indicated Harris’ nomination provided a bump in the polls for the democrats. Since President Biden announced he would abandon his bid for a second term, thirteen unique polls reflected Harris and Trump were one to three points apart in each poll3 (Trump led in eight polls while Harris led in five).

- Equity markets have generally been positive under the leadership of both parties: There have been 24 presidential elections dating back to 1928, U.S. equity returns averaged +11.0% in election years, slightly below the +11.6% average return in non-election years4. Since expanding to 500 stocks in 1957, the S&P 500 index has produced positive returns regardless of the party in power, the only exception being the 2001-2008 period that included the global financial crisis5. Presidential policy could affect equity markets in the short-term, but it may be unwise to make long-term investment decisions based on which party is in office.

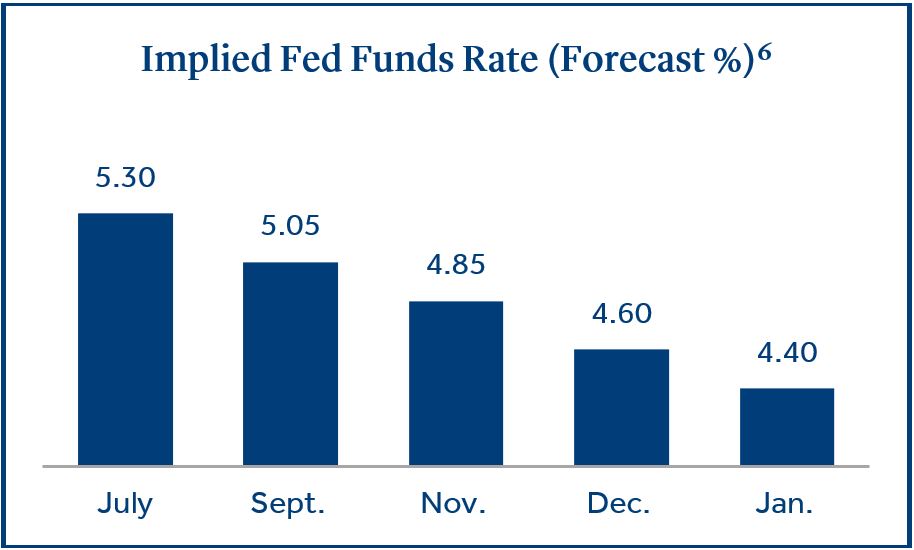

Federal Reserve

The Fed signaled it could lower interest rates in September if inflation remains subdued.

Strong job growth over the last year has allowed the Fed to be patient before cutting interest rates. However, job growth has trended lower alongside inflation in recent months. This prompted the Fed to acknowledge that risk to the labor market is now in balance with inflation, which could pave the way for the Fed to lower rates.

- The Fed left short-term rates unchanged at their July meeting: As expected, the Fed is waiting for further evidence that inflation is trending toward their 2% target. They will have two additional inflation reports (CPI) to review prior to their highly anticipated policy meeting in September.

- Interest rate futures are forecasting a 100% probability of a Fed rate cut in September6: Interest rates futures have priced in a near certain rate cut in September (-0.25%) and total cuts of -0.75% by January 20256. The most significant risk to a further delay in rate cuts would be higher than expected inflation.

- The election shouldn’t affect the Fed’s rate decision: Fed chair Jerome Powell has reiterated for some time the Fed will make interest rate decisions based on inflation and labor market data, while attempting to ignore the political landscape.

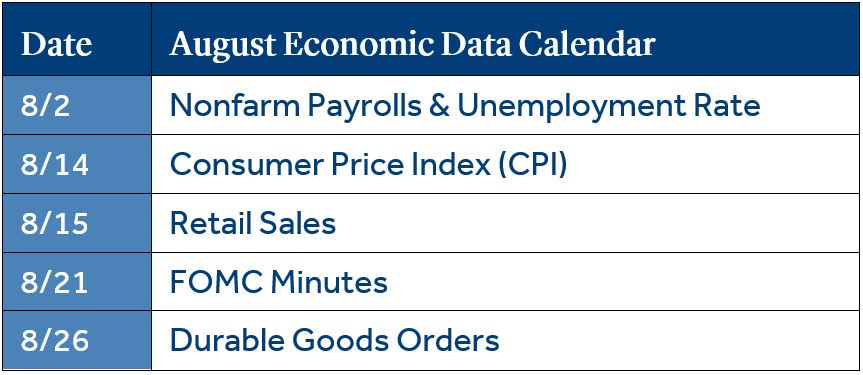

Economic Calendar

The U.S. economy is still growing, but new jobs and retail sales have softened.

- The U.S. labor market remained strong but new jobs have trended lower: The addition of +206K jobs in June topped forecasts (+200K) but new jobs in May were revised lower to from +272K to +218K. Monthly payroll gains in 2024 have averaged +222K, well above the +100K generally thought to reflect a growing economy. However, the three-month average has trended lower to +177K, the slowest pace since January 20217.

- Retail sales indicated consumers remained resilient: Retail sales were unchanged (0%) for the month, which was above expectations for a decline of -0.3%. Excluding autos, retail sales were positive +0.4% for the month. Retail sales remained positive (+2.3% annualized) but have steadily declined since December 2023 (+5.5% annualized).

- Inflation (CPI) continued to trend lower: CPI decreased -0.1% in June and was lower than expectations (+0.1%). Annualized inflation has declined for three consecutive months and now sits at 3.0%, matching the lowest level in over three years. Lower gasoline prices combined with lower automobile prices were the main catalysts for lower inflation.

To download the printable version, CLICK HERE.

Data and rates used were indicative of market conditions as of the date shown. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions and are subject to change without notice. This material is intended for general public use and is for educational purposes only. By providing this content, Park Avenue Securities LLC is not undertaking to provide any recommendations or investment advice regarding any specific account type, service, investment strategy or product to any specific individual or situation, or to otherwise act in any fiduciary or other capacity. Please contact a financial professional for guidance and information that is specific to your individual situation. Indices are unmanaged and one cannot invest directly in an index. Links to external sites are provided for your convenience in locating related information and services. Guardian, its subsidiaries, agents, and employees expressly disclaim any responsibility for and do not maintain, control, recommend, or endorse third-party sites, organizations, products, or services and make no representation as to the completeness, suitability, or quality thereof. Past performance is not a guarantee of future results.

Asset class returns sourced from Morningstar Direct. Asset categories listed correspond to the following underlying indices: Large Cap (S&P 500), U.S. Large Cap (S&P 500) Small Cap (Russell 2000), Non-US Dev (MSCI EAFE), Emerging Markets (MSCI EM), Bonds (Bloomberg US Aggregate Bond), Short Term (Bloomberg Short Treasury), Intermediate-term (Bloomberg US Treasury), IG Corp (Bloomberg US Corp. Bond), High Yield (Bloomberg High Yield Corporate), Global Agg ex-US (Bloomberg Global Agg Ex US – Hedged).

Treasury Yields sourced from the U.S. Department of the Treasury.

Inflation (CPI) sourced from the U.S. Bureau of Labor Statistics.

1 Source: Morningstar Direct

2 Source: William Blair

3 Source: Forbes

4 Source: T. Rowe Price

5 Source: Morningstar Direct

6 Source: Bloomberg / CME FedWatch Tool

7 Source: J.P. Morgan

S&P 500 returns under Democrat and Republican leadership represent the average annual return for each period.

The Consumer Price Index (CPI) examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care and is a commonly used measure of the rate of inflation.

Retail Sales represents the level of retail sales directly to U.S. consumers.

Durable Goods measure the cost of orders received by U.S. manufacturers of goods meant to last at least three years.

Fund Funds Rate: Short-term target interest rate set by the Federal Open Market Committee (FOMC); the policy making committee of the Federal Reserve. It’s the interest that banks and other depository institutions lend money on an overnight basis.

S&P 500 Index: Index is generally considered representative of the stock market as a whole. The index focuses on the large-cap segment of the U.S. equities market.

Russell 2000 Index: Index measures performance of the small-cap segment of the U.S. equity universe.

MSCI EAFE Index: Index measures the performance of the large and mid-cap segments of developed markets, excluding the U.S. & Canada.

MSCI EM Index: Index Measures the performance of the large and mid-cap segments of emerging market equities.

Bloomberg US Aggregate Bond Index: Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS, ABS, and CMBS.

Park Avenue Securities LLC (PAS) is a wholly owned subsidiary of The Guardian Life Insurance Company of America (Guardian). 10 Hudson Yards, New York, NY 10001. PAS is a registered broker-dealer offering competitive investment products, as well as a registered investment advisor offering financial planning and investment advisory services. PAS is a member of FINRA and SIPC.

2024-179036 (Exp. 08/26)