Monthly Market Commentary - February 2024

Monthly Market Commentary - February 2024

Market Update

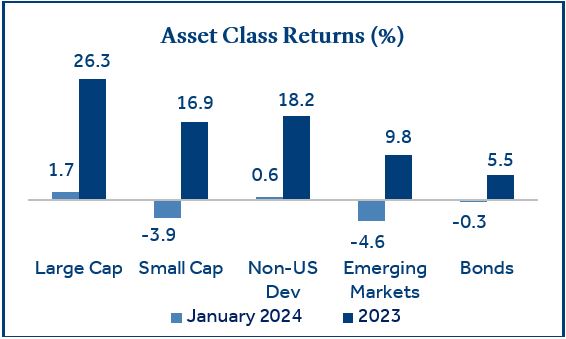

U.S. large cap stocks continued to lead asset class returns in January.

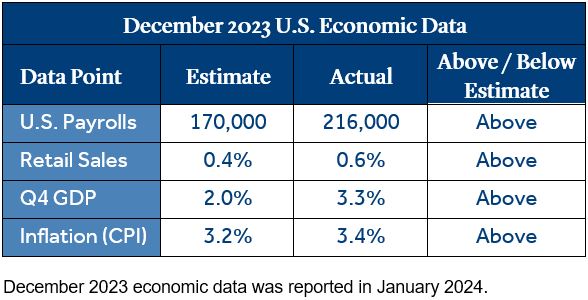

Economic data was primarily positive during the month as U.S. payrolls, retail sales, and Gross Domestic Product (GDP) all topped expectations. However, concerns that the Federal Reserve (Fed) may be less inclined to lower interest rates amid economic strength weighed on returns.

- U.S. Stocks: Large-cap stocks (S&P 500 Index) returned +1.7% and outperformed small-cap stocks (Russell 2000 Index) which returned -3.9%, as investors gravitated back to the popular mega cap stocks.

- Bonds: Bonds declined -0.3% as higher than expected inflation (CPI) pressured longer-term yields; the 10-year Treasury yield increased by +0.11% in January.

- Non-U.S. Stocks: Developed market stocks (MSCI EAFE Index) returned +0.6% and outperformed Emerging Markets stocks (MSCI EM Index), which returned -4.6% as Chinese equities (-10.6%) weighed on EM returns.

2024 Asset Manager Outlook

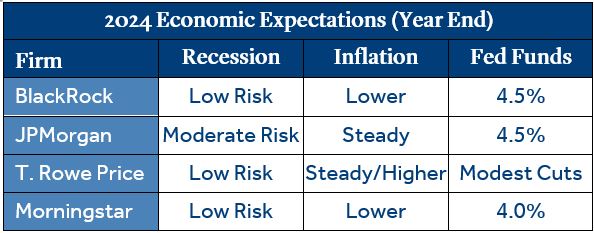

Many asset managers see a low to moderate risk of a recession in 2024.

As we move into the new year investors continue to grapple with the possibility of a recession as well as uncertainty around central bank policy, interest rates, and higher equity valuations. Several leading asset management firms (BlackRock, JPMorgan, T. Rowe Price, and Morningstar) recently released their 2024 outlooks which are highlighted below:

- Key Takeaways: The consensus view is that a resilient labor market and strong consumer trends are likely to keep the U.S. out of a recession. A pivot to less restrictive Fed policy is likely underway, but JPMorgan believed inflation could be stubborn and investors expecting rate cuts early in the year may be disappointed.

- Key Risks: Most believe that restrictive Fed policy and higher interest rates may not have fully permeated the economy. BlackRock was concerned that if economic growth slows, central banks won’t have the wide array of tools they’ve had in the past to respond. In addition, they see unusually high election uncertainty, as 50% of the global population is expected to vote in 2024.

- Equity Valuations: The group believes that equities overall may be near or slightly above fair value. T. Rowe Price pointed to opportunities in Emerging Markets, while Morningstar believed valuations are most attractive for domestic small cap stocks. However, lower interest rates and the absence of a recession may be key for these asset classes to excel.

China

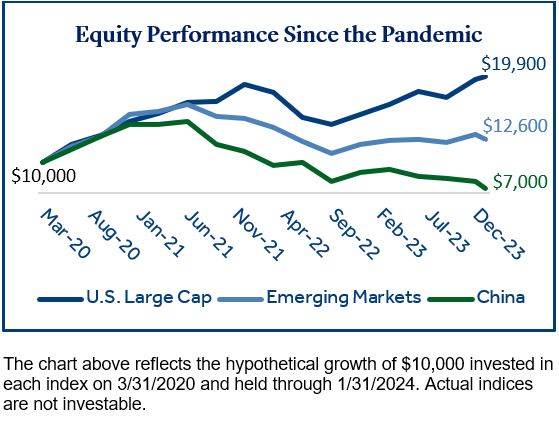

Chinese economic data continues to underperform post-pandemic.

China has struggled to recover economically from the COVID-19 induced decline. Three years of lockdowns during the pandemic have contributed to slower economic growth. Further, a growing real estate crisis has also weighed on growth as GDP increased only +5.2% in 2023, well below the 20-year average of +8.2%1.

- Economic Policy: As economic strain has increased, policymakers have taken several measures to stimulate economic growth. An infrastructure spending package was passed in October 2023 and reserve requirements for banks were cut in January 2024. Additional measures over recent days include loosening requirements for home buyers and broader aid for land developers.

- Equities: Mainland China and Hong Kong stock indices have been amongst the worst performers post-pandemic, with the latter reaching levels recently not seen since 1997.

- Valuations: Chinese stocks returned -8.4%, annualized since March 2020, which has led to a lower price-to-earnings (P/E) valuation. The current P/E ratio for Chinese stocks is 10.5, compared to 13.1 for Emerging Markets (MSCI EM Index) and 23.6 for U.S. large caps (S&P 500 Index).

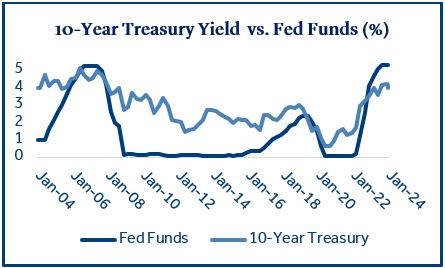

Federal Reserve

The Fed held short-term interest rates steady at the January meeting.

The decision to leave rates unchanged was widely anticipated by investors. The narrative has changed since the last policy meeting in mid-December when comments from Chairman Powell framed against forecasts for slowing economic growth and inflation likely accelerated rate cut expectations. However, better-than-expected economic data in December appears to have tempered expectations for now.

- Inflation (CPI): Consumer prices increased in December and CPI has been relatively flat over the past six months. It’s proven difficult for the Fed to generate consistently lower CPI with inflation currently in a range of 3-4%.

- Federal Funds Rate: The futures market is currently forecasting a 40% probability the initial Fed rate cut will be in March and a 90% chance the Fed Funds rate will end the year in a range of 3.75%-4.25%2.

- Fed Meeting: Chairman Powell’s comments at the post-decision press conference centered around the “balance of risks”. With economic activity expanding at a solid pace, the Fed will need to reach a higher level of confidence inflation is moving sustainably toward its 2% target before lowering rates.

The Fed may exercise caution prior to initiating their first rate cut. Recent events in the Middle East (oil rose +6.1% in January) and better-than-expected U.S. economic data both have the potential to be a catalyst for higher inflation.

Money Market

Money market funds experienced heavy inflows in 2023 as the Fed Funds rate approached a 20-year high.

Money market yields are highly correlated with the Fed Funds rate. As we shift into a different interest rate regime, money market funds could reflect rate changes quickly, potentially exposing fundholders to reinvestment risk.

- Money Market Flows: Investors poured over one trillion dollars into money market funds in 20233. Further, total money market assets have nearly doubled over the past five years, increasing from $3.1 trillion in late 2018 to $6.1 trillion in late 20234.

- Short-Term Rates: It is likely we are nearing the end of the Fed’s current rate hike cycle as the policy making committee is projecting three rate cuts in 2024. History indicates that once the Fed pauses, rate cuts tend to happen within months, as opposed to years, and cuts tend to happen rapidly5.

- Bond Yields: Intermediate-term yields are at levels not seen since 2007 and they tend to be uncorrelated with short-term rates. If you are in the camp that believes the Fed will begin cutting short-term rates in 2024, there could be an opportunity to lock in longer maturity yields at levels that have been unavailable for almost two decades.

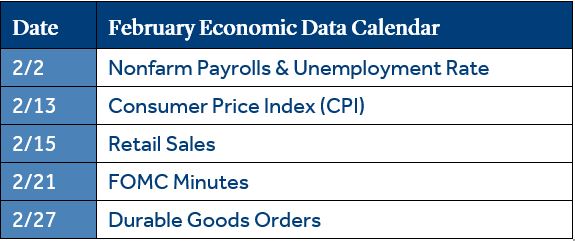

Economic Calendar

Nonfarm payrolls and corporate earnings are likely to be highlighted in early February.

The economic calendar is light in the first half of February, but fourth quarter corporate earnings will pick up during this time and could receive the bulk of attention from investors.

- Corporate Earnings: Earnings reports are in full swing as we enter February with most mega cap tech companies already reporting. Early indications are that earnings held up well even in the current higher interest rate environment. Continued earnings growth in 2024 will be crucial for equities to continue marching higher.

- Nonfarm Payrolls: Estimates are for +180k new jobs in January. Revisions (adjustments to the previous month) have been receiving attention recently as they have been mostly negative of late. October jobs were revised lower from 150k to 105k, and November was revised from 199k to 173k6.

- Inflation (CPI): Investors will be looking for a tick down in CPI after the upside surprise in December data. The Fed will see two more inflation reports prior to the highly anticipated policy meeting in March where some pundits believe the Fed may cut rates.

Data and rates used were indicative of market conditions as of the date shown. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions and are subject to change without notice. This material is intended for general public use and is for educational purposes only. By providing this content, Park Avenue Securities LLC is not undertaking to provide any recommendations or investment advice regarding any specific account type, service, investment strategy or product to any specific individual or situation, or to otherwise act in any fiduciary or other capacity. Please contact a financial professional for guidance and information that is specific to your individual situation. Indices are unmanaged and one cannot invest directly in an index. Links to external sites are provided for your convenience in locating related information and services. Guardian, its subsidiaries, agents, and employees expressly disclaim any responsibility for and do not maintain, control, recommend, or endorse third-party sites, organizations, products, or services and make no representation as to the completeness, suitability, or quality thereof. Past performance is not a guarantee of future results.

Asset class returns sourced from Morningstar Direct. Asset categories listed correspond to the following underlying indices: Large Cap (S&P 500), U.S. Large Cap (S&P 500) Small Cap (Russell 2000), Non-US Dev (MSCI EAFE), Emerging Markets (MSCI EM), Bonds (Bloomberg US Aggregate Bond), China (MSCI China), Oil (Bloomberg Sub WTI Crude Oil).

Treasury Yields sourced from the U.S. Department of the Treasury.

1 Source: Macrotrends

2 Source: CME FedWatch Tool

3 Source: Bank of America

4 Source: Federal Reserve Bank of St. Louis

5 Source: Amundi Asset Management

6 Source: U.S. Bureau of Labor Statistics

Durable Goods measure the cost of orders received by U.S. manufacturers of goods meant to last at least three years.

Retail Sales represents the level of retail sales directly to U.S. consumers.

The Consumer Price Index (CPI) examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care and is a commonly used measure of the rate of inflation.

Fund Funds Rate: Short-term target interest rate set by the Federal Open Market Committee (FOMC); the policy making committee of the Federal Reserve. It’s the interest that banks and other depository institutions lend money on an overnight basis.

S&P 500 Index: Index is generally considered representative of the stock market as a whole. The index focuses on the large-cap segment of the U.S. equities market.

Russell 2000 Index: Index measures performance of the small-cap segment of the U.S. equity universe.

MSCI EAFE Index: Index measures the performance of the large and mid-cap segments of developed markets, excluding the U.S. & Canada.

MSCI EM Index: Index Measures the performance of the large and mid-cap segments of emerging market equities.

Bloomberg U.S. Aggregate Bond Index: Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS, ABS, and CMBS.

Park Avenue Securities LLC (PAS) is a wholly owned subsidiary of The Guardian Life Insurance Company of America (Guardian). PAS is a registered broker-dealer offering competitive investment products, as well as a registered investment advisor offering financial planning and investment advisory services. PAS is a member of FINRA and SIPC.

2024-168433 (Exp. 02/26)

PAS018153