Monthly Market Commentary - January 2024

Monthly Market Commentary - January 2024

Market Update

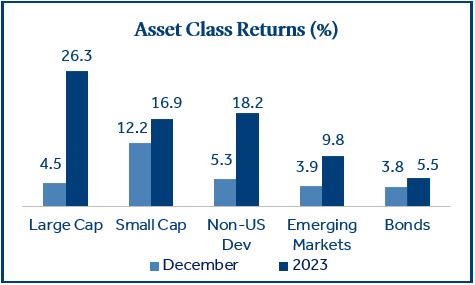

Small cap stocks lead strong asset class returns in December.

Capital markets posted strong year-end gains against a backdrop of lower inflation, a paused Federal Reserve (Fed), and a strong labor market.

- U.S. Stocks: Large-cap (S&P 500 Index) and small-cap stocks (Russell 2000 Index), were both up solidly in December, returning +4.5% and +12.2%, respectively.

- Bonds: Bonds returned +3.8% and posted their second strongest month of the year as the 10-year Treasury yield declined -0.49%.

- Non-U.S. Stocks: Developed market (MSCI EAFE Index) equities (+5.3%) outperformed Emerging Markets (MSCI EM Index) equities (+3.9%) as China (-2.4%) continued to weigh on EM returns.

Equity market breadth was also solid to finish the year. In addition to the strong outperformance by small cap stocks in December, the S&P 500 Equal Weighted Index (+6.9%) outperformed the S&P 500 Index by +2.3% during the period.

2023 Market Themes

Risk assets rebounded sharply in 2023 with U.S. large cap technology stocks outperforming.

Several themes unfolded throughout 2023 that dictated investor outcomes in the U.S. Despite the early volatility triggered by a regional banking crisis and a U.S. Treasury downgrade, U.S. large-cap stocks returned 26.3% by year end. Some of the key underlying trends in 2023 included the following:

- Technology Sector Drives Index Returns: The largest seven stocks in the S&P 500 Index returned +110% in total in 2023. This group is dominated by technology stocks such as Microsoft, Apple, and Alphabet. Technology was the top performing sector in the index, returning +57.8%.

- Growth Stocks Have Historic Year: Led by technology and consumer-oriented equities, growth stocks (+42.7%) outperformed value and dividend-oriented stocks which returned +11.5% and +10.7%, respectively. The performance difference between growth and value was the widest since 2020.

- Higher Yields Attract Investors: Although rising interest rates are generally negative for bond returns, yields rose less in 2023 than during 2022, providing a backdrop for positive returns. Investors preferred bonds with less interest rate sensitivity such as high yield bonds (+13.5%) which outperformed investment grade bonds (+5.5%) in 2023.

Commodities

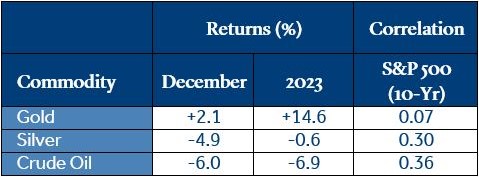

Commodities post mixed returns in December and 2023.

Commodities may offer correlation benefits when included in diversified investment portfolios as they tend to react differently to economic changes and geopolitical events than traditional asset classes. Commodities’ returns were mixed in 2023 but may be poised for a rebound as the Fed looks to reshape its interest rate policy in 2024.

- Precious Metals: Gold and silver returns were mixed in 2023, although neither metal kept pace with the broader equity markets. Fed interest rate hikes have held precious metals prices in check despite the tailwind of higher inflation. More recently, the Fed’s dovish pivot has breathed new life into spot gold prices.

- Energy: Crude oil faced headwinds in 2023 (-6.9%) due to economic growth concerns in the U.S. and China. Investors continue to monitor shipping challenges in the Red Sea related to the Israel-Palestine war as the outcome has the potential to drive oil prices.

Although commodities may offer diversification benefits to a portfolio, investors should be aware of the unique performance drivers relative to other asset classes.

Cryptocurrency

The Securities and Exchange Commission (SEC) could approve “spot bitcoin” ETFs in January.

Investors are closely monitoring the SEC as the regulator evaluates as many as 13 applications to launch new “spot bitcoin” ETFs. It is reported that discussions between the SEC and asset managers such as Blackrock, VanEck and Fidelity are progressing, signaling that the first spot bitcoin ETFs could be approved in early January. This raises several questions as investors consider the implications of this potential new investment vehicle.

- What are Spot Bitcoin ETFs? Spot ETFs would offer direct exposure to the price of bitcoin, as they would hold/store the physical bitcoin as an underlying position.

- When Would These Products Launch? If certain proposed spot bitcoin ETFs are approved in early to mid-January, some ETFs could be launched by asset managers as early as late January.

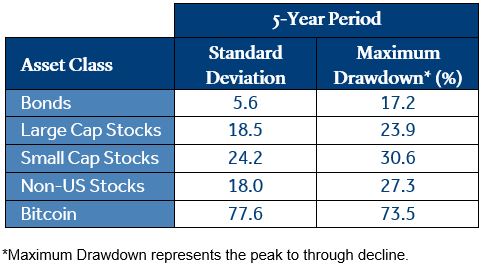

- Is Bitcoin a Safe Investment? Bitcoin has gained popularity for its high return potential, but it remains a highly volatile “investment”. Large historical price fluctuations experienced by cryptocurrencies should be considered when making any investment decisions.

Park Avenue Securities is actively monitoring the situation with the SEC and its potential spot bitcoin ETF approvals. PAS will continue to provide updated information as it becomes available.

Federal Reserve

The Fed held short-term interest rates steady for the third consecutive meeting.

The Fed’s decision to hold rates steady in December was widely anticipated by investors. However, investors may have been surprised by the Fed’s “dovish” pivot as Chairman Powell highlighted slowing growth and inflation in his press conference. The following are key expectations for inflation and interest rates post-meeting:

- Fed Inflation Outlook: The Fed lowered its price forecasts and now expects core inflation at 2.4% in 2024 (vs. previous estimates of 2.6%)1.

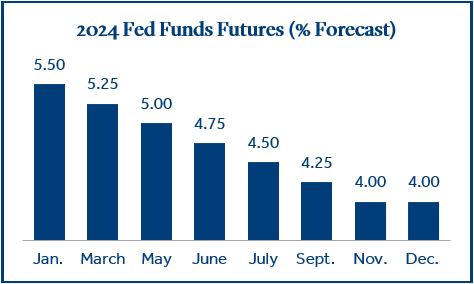

- Fed Rate Forecasts: Fed committee members are projecting three rate cuts during 2024. Interest rate futures have assigned a 70% probability the initial cut will be in March2.

- Fed Funds Futures: The futures markets are forecasting a series of interest rate cuts in 2024. Interest rate futures currently forecast a Fed Funds rate equal to or below 4.0% by December 20242.

Economic Calendar

Nonfarm Payrolls and inflation (CPI) will be in focus during the first half of January.

The economic calendar is evenly spaced in January with nearly a week between each highlighted data release.

- Nonfarm Payrolls: Investors will be paying close attention to job growth given the Fed’s comments that economic growth slowed during the fourth quarter. December estimates are for approximately 168k new jobs added3.

- Inflation (CPI): The December rally in stocks and bonds was largely based on the Fed dialing back inflation expectations. As such, it will be important for CPI (3.1%) to continue drifting lower toward the Fed’s 2% target.

- Retail Sales: A strong holiday shopping season, coupled with continued job growth, could lend further support to the soft-landing narrative for the U.S. economy. Early data showed that consumer spending was strong, increasing +3.1% in the period November 1 through December 244.

Data and rates used were indicative of market conditions as of the date shown. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions and are subject to change without notice. This material is intended for general public use and is for educational purposes only. By providing this content, Park Avenue Securities LLC is not undertaking to provide any recommendations or investment advice regarding any specific account type, service, investment strategy or product to any specific individual or situation, or to otherwise act in any fiduciary or other capacity. Please contact a financial professional for guidance and information that is specific to your individual situation. Indices are unmanaged and one cannot invest directly in an index. Links to external sites are provided for your convenience in locating related information and services. Guardian, its subsidiaries, agents, and employees expressly disclaim any responsibility for and do not maintain, control, recommend, or endorse third-party sites, organizations, products, or services and make no representation as to the completeness, suitability, or quality thereof. Past performance is not a guarantee of future results.

Asset class returns sourced from Morningstar Direct. Asset categories listed correspond to the following underlying indices: Large-cap (S&P 500), Small-cap (Russell 2000), Non-US Dev (MSCI EAFE), Emerging Markets (MSCI EM), Bonds (Bloomberg US Aggregate Bond), Value (Russell 1000 Value), Growth (Russell 1000 Growth), Bitcoin (S&P Bitcoin), Gold (LBMA Gold Price), Silver (LBMA Silver Price), and Crude Oil (Bloomberg WTI Crude Oil).

Treasury Yields sourced from the U.S. Department of the Treasury.

2024 Fed Funds futures forecast sourced from the CME FedWatch Tool.

1 Source: Federal Reserve

2 Source: CME FedWatch Tool

3 Source: Trading Economics

4 Source: Mastercard SpendingPulse

60/40 portfolio: Performance data was calculated using the S&P 500 Index (60%) and Bloomberg US Aggregate Bond Index (40%). Indices are uninventable.

Durable Goods measure the cost of orders received by U.S. manufacturers of goods meant to last at least three years.

Retail Sales represents the level of retail sales directly to U.S. consumers.

The Consumer Price Index (CPI) examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care and is a commonly used measure of the rate of inflation.

Fund Funds Rate: Short-term target interest rate set by the Federal Open Market Committee (FOMC); the policy making committee of the Federal Reserve. It’s the interest that banks and other depository institutions lend money on an overnight basis.

S&P 500 Index: Index is generally considered representative of the stock market as a whole. The index focuses on the large-cap segment of the U.S. equities market.

Russell 2000 Index: Index measures performance of the small-cap segment of the U.S. equity universe.

MSCI EAFE Index: Index measures the performance of the large and mid-cap segments of developed markets, excluding the U.S. & Canada.

MSCI EM Index: Index Measures the performance of the large and mid-cap segments of emerging market equities.

Bloomberg U.S. Aggregate Bond Index: Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS, ABS, and CMBS.

Park Avenue Securities LLC (PAS) is a wholly owned subsidiary of The Guardian Life Insurance Company of America (Guardian). PAS is a registered broker-dealer offering competitive investment products, as well as a registered investment advisor offering financial planning and investment advisory services. PAS is a member of FINRA and SIPC.

2023-166778 (Exp. 12/25)

PAS12601