Monthly Market Commentary - September 2023

Monthly Market Commentary - September 2023

Market Update

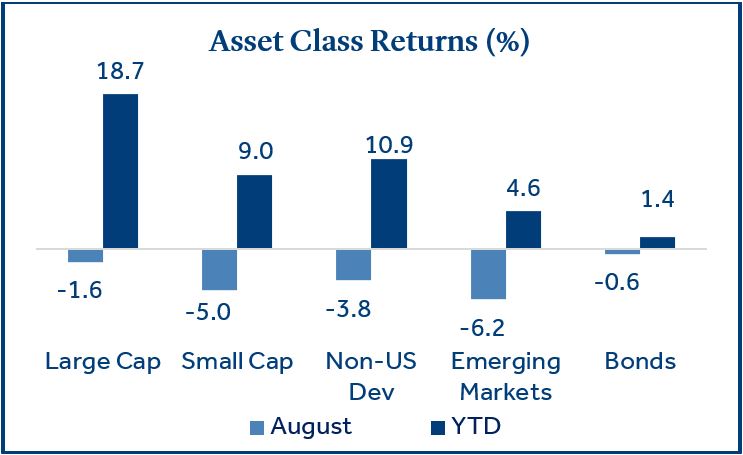

Major asset classes pulled back from recent highs in August.

Asset class returns were negative across the spectrum in August due to higher treasury yields and a hawkish tone from the Federal Reserve (Fed). Rising bond yields were in focus as the 10-year treasury yield increased from 3.97% to as high as 4.34%, before closing the month at 4.09%. Although inflation is trending lower, the Fed has made it clear their work is not finished and additional rate increases may be required. Against this backdrop, large-cap stocks (S&P 500 Index) and small-cap stocks (Rusell 2000 Index) declined, returning -1.6% and -5.0%, respectively. During the month, investors preferred the safety of large cap stocks relative to small cap stocks which have greater exposure to underperforming regional banks. Bonds started the year strong, but the tide has turned in recent periods. Bonds have now declined for four consecutive months, including -0.6% in August, as treasury yields have marched higher. Lastly, emerging markets stocks (MSCI EM Index) declined -6.2%, underperforming U.S. (S&P 500 Index) and non-U.S. developed market (MSCI EAFE Index) stocks as the economic recovery in China has disappointed.

Emerging Markets

Emerging Market equities have underperfomed as China's economic recovery falters.

Emerging Market equities (MSCI EM Index) have lagged developed markets (S&P 500 Index and MSCI EAFE Index) over multiple trailing periods as China has underperformed the broader index. After three years of COVID lockdowns and isolation, many expected the world’s second largest economy to see a strong rebound in 2023. China’s recovery got off to a strong start in the first quarter but since that time industrial production, retail sales, and real estate have all been under pressure.

Challenges facing China’s real estate market came to light in late 2021 when Evergrande Group, the country’s second largest property developer, defaulted on bond payments. More recently, issues resurfaced in China’s real estate sector in mid-August as another large developer, Country Gardens, sought to extend payment deadlines to avoid default. In addition, new home, and apartment sales for the top 100 developers in China dropped by -33% in June and July compared to a year ago1. Concerns of contagion are making it difficult for real estate developers to raise capital which could exacerbate the issue. China’s real estate market is estimated to directly and indirectly account for up to 25% of all domestic economic activity2. As a result, stabilization in the sector could be vital to an economic recovery and many expect the Chinese government to roll out additional policy support for the real estate market. Investors will be watching closely as it could be difficult for emerging markets to gather sustained momentum without China, which represents a 31% allocation in the MSCI EM Index.

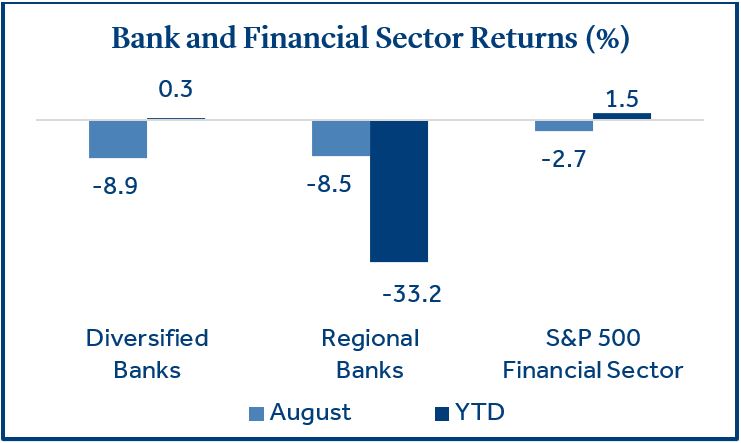

U.S. Banking Sector

Recent credit downgrades drove bank stocks lower during the month.

Standard & Poor’s (S&P), Moody’s, and Fitch all took aim at the U.S. banking sector in August. Moody’s commenced the deluge by downgrading 10 regional banks, assigning a negative outlook to 11, and placing an additional 6 under review3. Fitch, who received attention for their recent downgrade of U.S. long-term debt, stated that if rate hikes continue, they will be “forced” to review over 70 banks and will likely downgrade dozens, due to the negative effects of a higher fed funds rate and rising treasury yields on bank portfolios3. Lastly, S&P downgraded five mid-sized banks later in the month.

A challenging interest rate environment is driving credit concerns for several reasons. Among the challenges facing banks, higher rates are curbing the demand for new loans, an inverted yield curve (short-term rates higher than long-term rates) has made loans less profitable, and rising treasury yields are reducing the value of fixed income portfolios (balance sheets) for banks. As a result, bank equities experienced a broad decline in August, with smaller regional banks experiencing the brunt of the selling year-to-date.

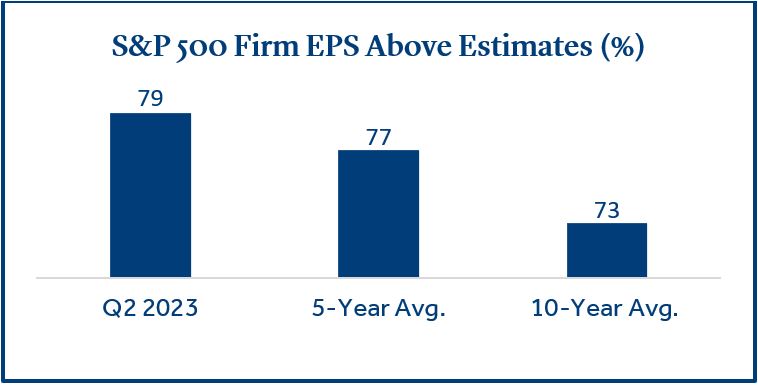

Corporate Earnings

Positive earnings surprises for the second quarter were above long-term averages in August.

Following the second quarter, 84% of S&P 500 companies have reported earnings with 79% reporting earnings per share (EPS) above analyst estimates. This data point is above the five and ten-year averages and represents the highest percentage of positive surprises since the third quarter of 2021 (82%)4. Eight of eleven S&P 500 sectors have reported year-over-year earnings growth with Consumer Discretionary and Communication Services leading the way, while Energy, Materials, and Health Care all declined.

This is welcome news for investors as many have anticipated a decline in corporate profits due to higher inflation and rising interest rates. From a valuation standpoint, the S&P 500 is trading with a price-to-earnings (P/E) multiple of 19.2 times forward earnings, which is slightly above the five- (18.6) and ten-year average (17.4)4.

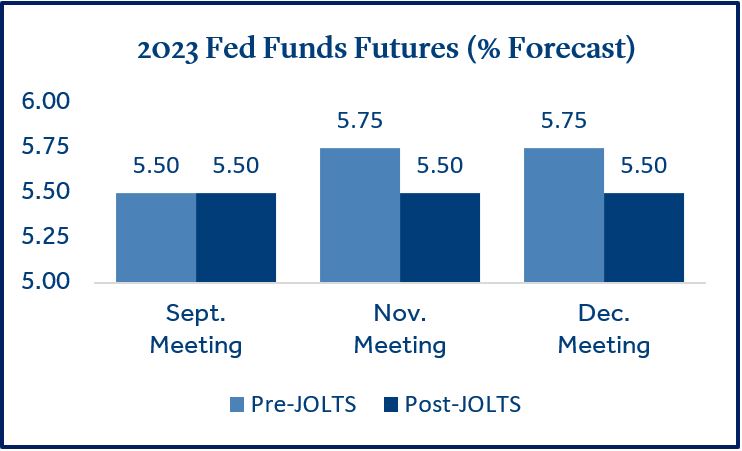

Federal Reserve

Fed Chair Jerome Powell stated the Fed is prepared to "raise rates further" if appropriate.

During the Fed’s annual symposium in Jackson Hole chairman Powell acknowledged the progress made against inflation but also reaffirmed it was above the Fed’s desired target of 2%. Inflation (CPI) steadily declined for 12 consecutive months from a peak rate of 9.1% in June 2022 to 3.0% in June 2023. However, CPI ticked up in July (3.2%) for the first time in over a year. It may prove more difficult for the Fed to consistently generate lower CPI with the current inflation rate hovering around 3%, versus comparisons against much higher rates over the past year.

Powell admitted there are risks to doing too much or too little from a policy perspective, but a strong economy and lower inflation should provide flexibility to proceed carefully. Following the speech, futures markets were initially forecasting one additional 0.25% rate hike in 20235. However, days later a weaker than expected JOLTS (Job Openings Report) reversed that forecast as it was surmised the Fed may hold short-term rates steady due to softening jobs data. Ultimately, investors may not be as concerned about another rate hike, as much as they are concerned that the Fed may keep rates at current levels for longer than originally anticipated.

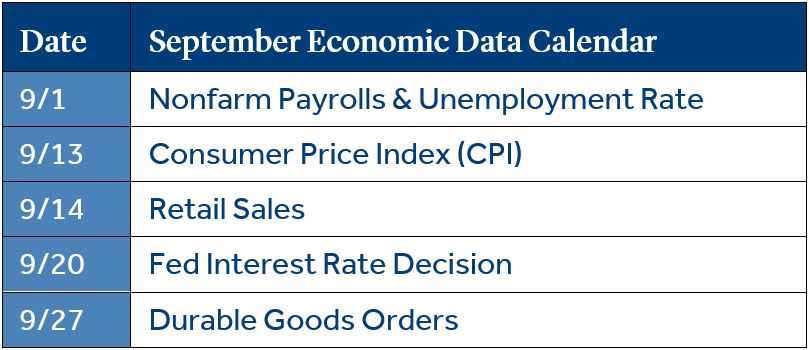

Economic Calendar

The Fed's interest rate decision could move markets late in the month.

We got a peek into September economic data as nonfarm payrolls and unemployment were reported on the 1st of the month. New jobs (187k) exceeded estimates (170k) but average hourly earnings (4.3%), a key data point for clues on the direction of inflation, was below forecasts (4.4%). In addition, unemployment increased from 3.5% to 3.8% as more individuals are looking for work.

CPI will be highly anticipated as it comes just a week before the next Fed rate decision. The inflation print will likely be heavily scrutinized given the slight increase we saw last month. The futures market is not currently forecasting a rate increase during the 9/20 Fed meeting, so a higher-than-expected CPI report has the potential to create volatility if it alters the forecast. The counterargument is that a soft inflation report on the heels of better-than-expected corporate earnings could open the door for a rebound in risk assets.

Data and rates used were indicative of market conditions as of the date shown. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions and are subject to change without notice. This material is intended for general public use and is for educational purposes only. By providing this content, Park Avenue Securities LLC is not undertaking to provide any recommendations or investment advice regarding any specific account type, service, investment strategy or product to any specific individual or situation, or to otherwise act in any fiduciary or other capacity. Please contact a financial professional for guidance and information that is specific to your individual situation. Indices are unmanaged and one cannot invest directly in an index. Links to external sites are provided for your convenience in locating related information and services. Guardian, its subsidiaries, agents, and employees expressly disclaim any responsibility for and do not maintain, control, recommend, or endorse third-party sites, organizations, products, or services and make no representation as to the completeness, suitability, or quality thereof. Past performance is not a guarantee of future results.

Capital Market Returns sourced from Morningstar Direct. Asset categories listed correspond to the following underlying indices: Large-cap (S&P 500), Small-cap (Russell 2000), Non-US Dev (MSCI EAFE), Emerging Markets (MSCI EM), Bonds (Bloomberg US Aggregate Bond), China (MSCI China), Diversified Banks (S&P 500 Diversified Banks industry), Regional Banks (S&P 500 Regional Banks Industry).

Treasury Yields sourced from the U.S. Department of the Treasury.

Durable Goods, Retail Sales, Nonfarm Payrolls, and unemployment rate data sourced from Trading Economics.

1 Source: S&P Global Ratings

2 Source: New York Times

3 Source: Forbes

4 Source: FactSet

5 Source: CME FedWatch Tool

Durable Goods measure the cost of orders received by U.S. manufacturers of goods meant to last at least three years.

Retail Sales represents the level of retail sales directly to U.S. consumers.

The Consumer Price Index (CPI) examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care and is a commonly used measure of the rate of inflation.

Fund Funds Rate: Short-term target interest rate set by the Federal Open Market Committee (FOMC); the policy making committee of the Federal Reserve. It’s the interest that banks and other depository institutions lend money on an overnight basis.

S&P 500 Index: The Index is generally considered representative of the stock market as a whole. The index focuses on the large-cap segment of the U.S. equities market.

Russell 2000 Index: Index measures performance of the small-cap segment of the U.S. equity universe.

MSCI EAFE Index: Index measures the performance of the large and mid-cap segments of developed markets, excluding the U.S. & Canada.

MSCI EM Index: Index Measures the performance of the large and mid-cap segments of emerging market equities.

Bloomberg U.S. Aggregate Bond Index: Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS, ABS, and CMBS.

Park Avenue Securities LLC (PAS) is a wholly owned subsidiary of The Guardian Life Insurance Company of America (Guardian). PAS is a registered broker-dealer offering competitive investment products, as well as a registered investment advisor offering financial planning and investment advisory services. PAS is a member of FINRA and SIPC.

2023-160809 (Exp. 08/25)